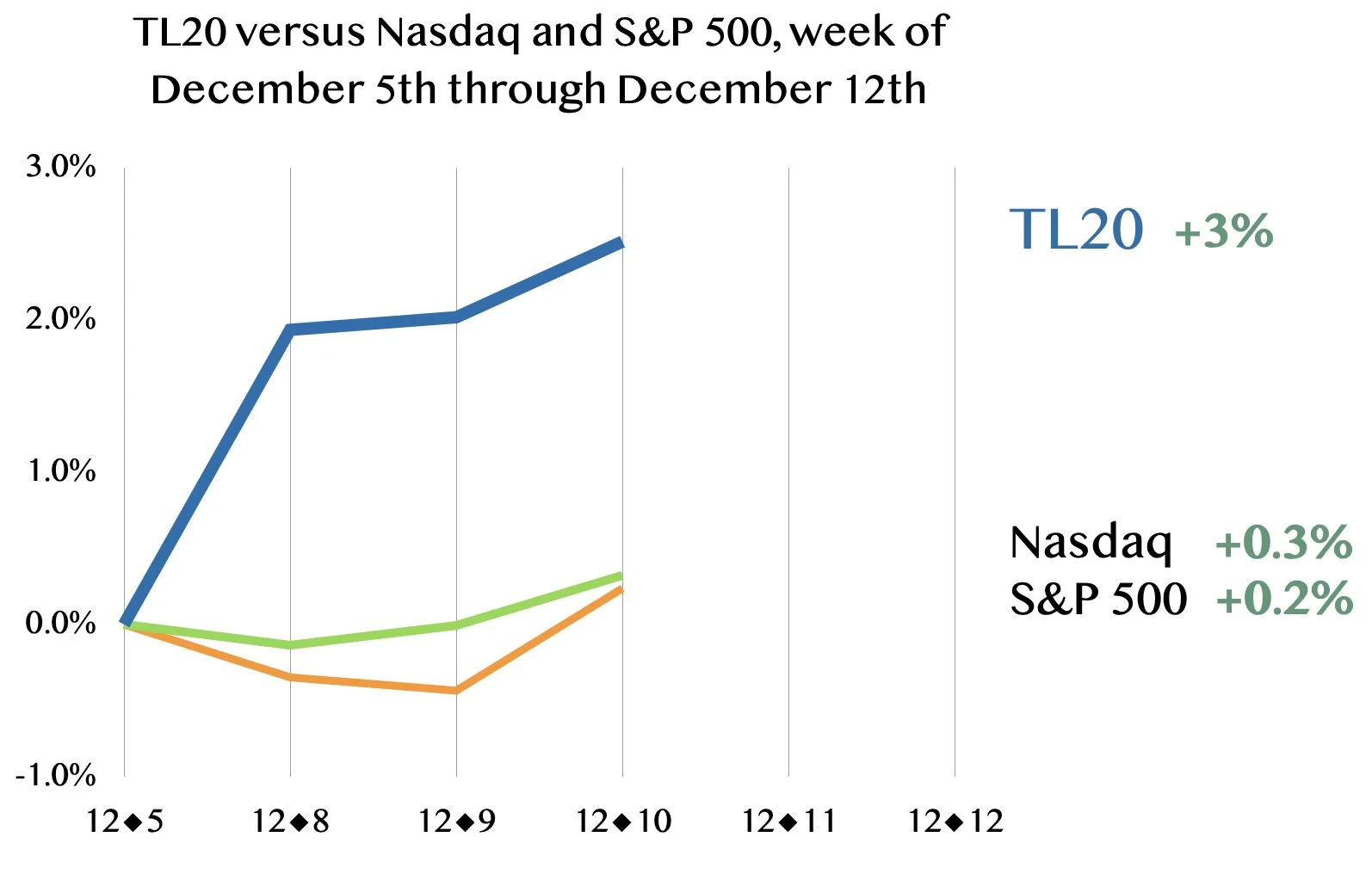

TL20 lags benchmarks

Year-to-date, the TL20 group of stocks to consider is up fifty-five percent, better than the twenty-two-percent gain of the Nasdaq and the seventeen-percent gain of the S&P 500. Read about the TL20

Take the poll: Are you interested in a TL20 ETF?

I hadn’t paid much attention to three-billion-dollar expense-management software maker Navan when it came public on October 30th in a billion-dollar offering lead by Goldman Sachs and Citigroup — which is just as well, as the stock has lost a third of its value from its first-day close of $20, and is down forty-five percent from the offer price, at a recent $13.85.

The company heads for its first-ever quarterly report on Monday, December 15th, and the Street is uniformly bullish on the software maker.

Navan mainly makes revenue from commissions paid to it by travel bookers when it directs business travelers to the bookers. There’s also an individual “per-transaction” fee direct from some customers, and a subscription fee for companies that use Navan’s expense-management software.

Some of this touches on something I didn’t know had a name: “Bleisure,” which is defined in its IPO prospectus by Navan as the “category of the business travel market defined by personal travel booked around or in connection with business travel.”

I’ve often thought International Business Machines is where things go to die, and another thing is going to that graveyard Monday morning, Confluent, the eight-billion-dollar maker of software to connect real-time events, which is being bought by IBM for a thirty-four-percent premium, at $31 in cash.

Confluent’s software, called “Kafka,” is used as a kind of connective tissue to let applications respond in real-time to events, such as a person clicking on a Web page. It was the force behind the feature on LinkedIn that tells you how many profile views you have, dating from back when Confluent CEO and founder Jay Kreps first wrote the Kafka code as an employee of LinkedIn. (More in my original profile of Kreps.)

Confluent has had mixed business results, and its stock has badly lagged the market for years now. My understanding is that the fundamental problems include the complexity of setting up a Kafka system for most enterprise IT, and also the fact that the early adopters tended to simply use the free, open-source version of Kafka rather than pay Confluent a fee.

I dropped Confluent from the TL20 group of stocks to consider in the February, 2024 rebalancing. Since that time, The TL20 is up 126% while Confluent is down two percent prior to this offer. Even with the thirty-four-percent premium, that would seem to make the decision the right one. You would have had to wait a long time to get bought out if you had stuck with Confluent.

“When you have a monopoly, you are in your own world […] And here, we created a very sophisticated system that now worries the Goliath.”

Software maker Snowflake’s drop of eleven percent on Thursday, to $235, following a decent fiscal third-quarter earnings report on Wednesday evening is a little like the twenty-six-percent plunge that Pure Storage took on Wednesday, which is to say, in my mind, it’s mostly about people taking profits.

The stock had been up seventy-six percent for the year heading into the report, after four quarters in which the stock jumped following each report, and a particularly strong second-quarter report that drove shares up back in August.

The proximate cause of the decline is that the company’s forecast was mixed. The projection for twenty-eight percent growth in Snowflake’s “product” revenue this quarter (the company never forecasts total revenue, as it leaves aside its services revenue) was higher than expected, but not as high as the “whisper” number. And the operating profit margin forecast of seven percent this quarter was below consensus for eight percent or higher.

Pure Storage is a stock that alternates between pretty stark increases and declines in stock price following earnings reports. Back in August, it saw a thirty-two-percent pop following its report. Wednesday, it’s a twenty-six percent plunge, dropping to $69.29.

The issue for Pure every single quarter is not the numbers, which continue to be very strong, it’s how much the company is going to sell to “hyperscale” clients, the cloud computing titans. So far, though CEO Charlie Giancarlo has repeatedly teased the prospect of deals for years now, Pure has only announced projects with Meta Platforms.

The sell-off today is that Giancarlo teased that he’s entertaining a variety of possible deal structures to lure more cloud clients, and one prospect is that Giancarlo will absorb up-front cost of NAND flash chips, the main ingredient, which could lower his gross profit margin — he’d take less profitable deals to win business, in other words.

“Our checks indicate that the new model can include PSTG procuring the NAND Flash directly from suppliers (Kioxia/MU) instead of only providing the software license,” as it does with Meta, writes Krish Sankar of TD Cowen.

We are still in the throes of a debate over an AI bubble. Skeptics point to the “circular” financing deals, optimists point to the raging demand in Nvidia’s most recent report.

Over the weekend, The Financial Times continued to dig into the details, with a story by Tabby Kinder and George Hammond pointing out that OpenAI has used its partners’ balance sheets to absorb some of the debt financing instead of OpenAI taking on that debt themselves.

Then, on Monday, another piece by Kinder and colleagues points out that OpenAI has taken a stake in private equity firm Thrive Holdings that is a non-cash swap: OpenAI will give Thrive’s portfolio companies access to OpenAI technologies, yet another instance of a circular deal.

I noted Monday the skeptical views about CoreWeave, the debt-laden AI hosting firm. MoffettNathanson warns of the risk to the company’s borrowing of having sub-prime customers such as OpenAI and Poolside AI, the French AI startup. They could drive up CoreWeave’s borrowing costs.

“Consumer demand of interactions with their brands, overall, is growing at double digits.”

Monday was the day for the analysts to weigh in for the first time on six-billion-dollar BETA Technologies, which came public on November 4th and has since lost a quarter of its value, dropping from its first-day close of $35 to $26.43, which is also below the IPO offer price of $34.

This is, I have to say, one of the more interesting IPOs in a while because they actually make stuff: Electric airplanes. The prospectus for IPO even looks cool because it has lots of pictures of electric planes.

The company raised a pretty good amount, $960 million, in the deal lead by Morgan Stanley and Goldman Sachs, and the coverage from the underwriters is almost uniformly positive today.

Eight-year-old BETA, which is based in South Burlington, Vermont, boasts that its planes, which have flown thousands of miles, including passenger flights into New York’s JFK airport, “represent a significant cost efficiency advantage,” the prospectus states. The “total operating costs are 42% lower compared to new traditional conventional aircraft based on internal estimates,” the company states.

Tuesday evening was a pretty terrible one for software, with shares of Nutanix, PagerDuty, Workday, and Zscaler selling off on mixed results. The stocks continued to fall hard during Wednesday’s regular session.

Dell Technologies was the saving grace Tuesday evening as its report showed some glimmers of hope in the company’s effort to make a profit off of AI servers. That was enough to drive the stock up six percent Wednesday.

A STRUCTURAL CHANGE FOR NUTANIX

Let’s start with the most disappointing report, Nutanix, which has been one of the TL20 stocks to consider since the September of 2023 rebalancing. The stock had been weak already this year, down four percent heading into Tuesday’s report. It closed down Wednesday by eighteen percent, at $48.34.

The proximate cause for the sell-off was the company missing with its revenue for its fiscal first-quarter ended in September, and cutting its full-year outlook for revenue.

Among Tuesday’s earnings winners is TL20 stock to consider Analog Devices, which beat expectations with both reported results and its outlook, sending shares up four percent at $249.05.

Among other winners Tuesday is Symbotic, the maker of robotics systems for warehouse automation, which is up thirty-six percent at $75.50. Symbotic had already been up a hundred and thirty-four percent heading into the report, so this is adding to massive gains already.

Symbotic is the result of a $4.5 billion takeover in 2022 of what had been Warehouse Technologies LLC., a private startup partly owned by Walmart, which was taken public in a reverse merger with one of SoftBank Group’s “special-purpose acquisition companies,” or, SPAC, a “blank check company,” back when SPACs were very, very active.

Symbotic tends to rise every other report, meaning, it flip-flops between big losses and big gains. In August it plummeted fourteen percent, today, it’s up much more than that.

The week ending November 21st ended with a thud for tech stocks, the Nasdaq Composite Index declining by three percent as the earnings report of Nvidia brought stunning results, but no answer to the question of whether we are in an “AI bubble.”

The newspapers are making the topic front-page news again. The New York Times’s Cade Metz seems only now to have caught up with the AI bubble concerns, in a broad piece Monday morning. He notes “something ominous lurking behind all this bubbly news,” including the massive investment plans and the lack, so far, of any clear productivity gains from AI. Metz adds little that’s new, really.

Let’s go back to when Nvidia’s Jensen Huang reported earnings results on Wednesday the 19th. The reported numbers, and the outlook for this quarter’s revenue, were both stunning. But Huang failed to really address the bubble concerns.

Nvidia shares gave up their earlier gains on Thursday, closing down three percent at $180.64, as the Street had to reconcile the persistent fears of an AI bubble with the simply stellar results from the company.

I didn’t think CEO Jensen Huang did a good job addressing concerns of an AI bubble. Frankly, I thought he ignored the questions of whether there is a looming funding gap, and to what degree financing is “circular.”

But the Street is generally a lot less worried than I am. The view from the analysts covering the stock is that as long as the business is humming along, which it is, worries of a bubble get kicked down the road.

“No AI Bubble Here, At Least Not Yet,” writes Craig-Hallum’s Richard Shannon, who has a Buy rating on the stock, and a $245 price target.

Nvidia shares are rising in the pre-market Thursday morning, and estimates and price targets are once again rising as the company pulled another rabbit out of the hat, delivering the $65 billion revenue forecast for the current quarter that was the “whisper number” the company had to hit. Gross profit margin also is holding up astoundingly well despite massive investment in materials and inventory.

Given just how stellar those results are, one could excuse CEO Jensen Huang for both raising the topic of an artificial intelligence “bubble” and then failing to actually address the concern.

With each passing week, the enormity of investment in artificial intelligence becomes more striking, and the risk seems to rise as well.

Some are finally stepping back and downgrading their view of Mega-Cap Tech.

“It is time to take a more cautious stance on the hyperscalers and move beyond the industry’s reassuring ‘trust us – Gen-AI is just like early cloud 1.0’ narrative, which looks increasingly misplaced,” writes analyst Alex Haissl of Rothschild & Co. Redburn on Tuesday.

Haissl cut his ratings on Amazon and Microsoft to Neutral from Buy. His main contention is that the capital burden on these firms is a lot bigger than it was in what he calls “Cloud 1.0,” which was the cloud computing era that began in 2006 when Amazon first turned on its “AWS” cloud computing service. Amazon and Microsoft are the two biggest of the Big Three cloud computing operators, ahead of Alphabet’s Google.

Privately held artificial intelligence developer Anthropic, which has gotten $31 billion in funding from Amazon, Alphabet, and numerous venture capitalists since 2021 — including an “F” round two months ago — on Tuesday received pledges of billions more from both Nvidia and Microsoft.

In the latest instance of “circular” financing, as many are calling the customer-vendor deals, Microsoft announced that Anthropic has committed to spending $30 billion on Microsoft’s Azure cloud services, and that Microsoft will invest “up to” $10 billion in Anthropic and Nvidia will invest $5 billion.

The Anthropic spending is earmarked for use of Nvidia chips in Azure, said Microsoft, adding, “Anthropic’s compute commitment will initially be up to one gigawatt of compute capacity with NVIDIA Grace Blackwell and Vera Rubin systems.” Anthropic had its own press release on the deal.

Following the announcement, CNBC’s MacKenzie Sigalos reported that Anthropic is now valued at $350 billion, up from the $183 billion at which the F round valued the company in September.

“As much as we read about some of the hype around AI, the reality is, at the SMB level, the value is very, very real.”

Two heavy weeks of earnings reports have left stocks lower, the Nasdaq Composite Index closing down half a point the week ending November 14th, and five percent the week before. That is likely because of stocks hitting new 52-week and all-time high prices.

I compiled a list of thirty-two stocks that had the biggest declines and gains in the days and weeks following their earnings reports.

Shares of chip equipment giant Applied Materials are up fractionally on Friday at $225.01 following Thursday evening’s earnings release — the first gain on earnings following six quarters of sharp sell-offs. The last report, in August, the stock sold off by the most in over a decade.

The ray of hope this time around is that the company’s forecast for quarterly sales finally topped expectations after four quarters in a row of disappointment.

But Applied is still in a sense in uncharted waters. The issues have been uncertainty related to the effects of tariffs and restrictions on sales to China. The tariff fears have eased for the moment, given detente between the U.S. and China; but the company is definitely going to sell less to China going forward, though it’s hard to say how much less.

The larger issue, as I explained in August, is what I call “The Taiwan Semi Effect,” the company’s dependence on Taiwan Semiconductor Manufacturing as the most dominant of its customers. That is making business less predictable than in past for Applied’s sales.

Everyone loves a potentially new way to play the artificial intelligence trade, and shares of Cisco Systems are up four percent Wednesday on just a glimmer the company might be the latest vendor caught in a rush of investment for AI.

That’s noteworthy because Cisco is a cheap stock. At $77.32, it trades for five times this year’s projected revenue, and nineteen times possible EPS.

There’s some debate, however, over what to make of Wednesday evening’s outlook.

The headline news is that the company lifted its revenue forecast for the fiscal year that ends next July by a billion dollars, to $6.6 billion, give or take four hundred million. That would represent a rate of growth of 6.5%. Maybe that doesn’t sound like much, but it is a big relief Thursday to bulls on the stock who had been agitated back in August that the year outlook was for merely five percent growth.

One of those worriers back in August, Rosenblatt Securities’s Mike Genovese, is reassured. “This Cisco quarter made us more positive on the name than before,” he writes, reiterating a Buy rating and hiking his price target to $100 from $87.

“The beauty is, he's built a business that's bigger, and scaled much greater, than Procore. He knows what he's doing, that's for sure.”

Advanced Micro Devices is a company that for a long time couldn’t get any credit as a credible competitor to Nvidia in AI chips. All that changed on October 5th when the company struck a deal with OpenAI to a massive amount of AMD chips, in return for OpenAI taking a stake in AMD.

Shares of AMD soared by twenty-four percent the next day, and since that time, they are up seventeen percent at a recent $237.52.

Tuesday was the coda to the October announcement, as AMD CEO Lisa Su and her executives took the stage in New York for an “analyst day” event, the dog & pony show where a company discusses long-term product strategy, market outlook, and some financial goals.

The headline from the five hours of proceedings was one trillion dollars. That is the amount of the annual addressable market that is related to artificial intelligence that Su foresees in 2030.

Shares of artificial intelligence data center operator CoreWeave are slumping by eight percent in early trading at $97.04, after the company delivered results Monday night that topped expectations but also cut its outlook for 2025, citing a delay in a third party that was helping CoreWeave assemble one of its data center “shells,” the basic physical structure of the facility.

This is only the company’s third report since it went public in March, and the first report since CoreWeave called off its proposed acquisition of Core Scientific. The stock was up 164% since the IPO heading into Monday night’s report.

Both bull and bear are taking the shortfall in stride.

It’s been a year and a half since I interviewed Paddy Srinivasan as he took the reins at software maker DigitalOcean. The challenge for Srinivasan was to turn around a company that had seen growth dramatically slow in 2024, sending its stock into a tailspin.

It looks like Srinivasan’s efforts are working. DigitalOcean stock is up fifty-four percent this year at a recent $51.93.

Growth has picked from last year, projected at almost fifteen percent this year versus twelve percent in 2024, and the stock is winning new fans.

Following last Wednesday’s upbeat earnings report, the shares soared eighteen percent, the second quarter in a row the stock saw a double-digit gain.

One new fan is Oppenheimer & Co.’s Param Singh, who initiated coverage on Monday with an Outperform rating, and a $60 target, which would be about sixteen percent from here.

Welcome to the end of a week of over a hundred tech earnings reports of some significance. While I’m not covering each one exhaustively, I think we can say some things in broad strokes about what’s working and what’s not.

Based on the table at the bottom of the post, there are some definite trends here.

BEING SUB-SCALE IS NO BUENO

First, the losers.

Being a “sub-scale” vendor in the advertising market, meaning, not having the influence of Google or Meta that comes from being much bigger, is not a great place to be. You can see that in the muted response to decent reports from DoubleVerify and The Trade Desk and Yelp.

There are other places where it is bad to be sub-scale. Being a smaller, focused chip-equipment vendor such as Onto Innovation is proving not as rewarding as being one of the giants such as Lam Research, KLA, BE Semiconductor or ASML.

The latest sign of the strong Street interest in quantum computing was a packed audience Wednesday at the Nasdaq for a product unveiling by Quantinuum, a division of industrial giant Honeywell.

Quantinuum is probably the best-known private company in the quantum race, while most of the Street’s attention is typically focused on the three public “pure plays,” IonQ, D-Wave, and Rigetti. (IonQ and D-Wave both reported upbeat quarterly results this week.)

Quantinuum CEO Rajeeb Hazra told the crowd that the new “Helios” machine marks the company’s achievement of the “first commercial-grade quantum computer.” The hour and a half of discussions with Hazra, with customers, and with an executive from partner Nvidia were moderated by CNBC anchor Morgan Brennan and by Alix Steel, a former Bloomberg reporter now a principal at a consultancy called DrivePath advisors.

The choice of the two moderators was unfortunate as the duo seemed not to know very much at all about quantum, and the questions were all softball types. Well, that’s to be expected from a product “launch,” I suppose.

The hits keep coming in yesterday and this morning’s earnings reports. Here’s just a sample. See the table at the bottom of the post for the complete rundown.

Fiber-optic giant Coherent is surging eighteen percent in pre-market trading, reversing the big sell-off that happened to the company with the August report. Among the highlights, the company’s revenue forecast for the quarter, nearly five percent above consensus, is the most upside in years.

Coherent’s report adds fuel to the fiber-optic outlook following on the heels of Tuesday’s upbeat report from smaller competitor Lumentum.

The highlight is, of course, sales of transceivers into data centers, driven by the raging cloud and AI nature of things. On the call, CEO James Anderson said the company is “experiencing exceptionally strong demand.” Sales for that part of the business rose twenty-three percent, year over year, faster than the nineteen percent level of total revenue.

With tech stocks hitting new all-time highs lately, and with a massive sell-off of the market on Tuesday, on fears of artificial intelligence bubble spending, it is perhaps no surprise that some perfectly fine reports on Tuesday evening were greeted with further selling. (See the table of reports at the bottom of the post.)

Arista Networks is one of the names that sold off hard, down seven percent in early trading Wednesday, at $142.10, despite beating expectations Tuesday evening for the September quarter, and forecasting this quarter higher as well.

The consensus is that the Street wanted Arista to raise its outlook for 2026 and it didn’t, so that was disappointing.

“The negative stock reaction post close reflects the reality that forward estimates are not moving up in a material manner,” writes Amit Daryanani of Evercore ISI, who has an Outperform rating on the shares, and a $175 price target.

“ANET maintained their expectation of 20% sales growth in CY26 though off a higher revenue base vs. 90-days ago (implicitly CY26 dollar revenues are revised higher).”

Simon Leopold of Raymond James, who has a Market Perform rating on the stock, writes similarly that the stock drop “we think resulted from elevated expectations and no real fundamental shift.”

The artificial intelligence trade can make some people do crazy things, like buying shares of a stock trading for ninety-two times projected sales, as in the case of Palantir Technologies.

The shares are down over seven percent, pre-market, at $192.16, despite an upbeat report and forecast Monday evening that just wasn’t enough for a stock this richly valued.

This is basically a repeat of what happened back in May, when results were also pretty stellar but the stock sold off by twelve percent. It’s what happens when a high-performing company has an over-valued stock.

Why might Palantir deserve such a rich stock price? The numbers, themselves are certainly nice. The eight-percent surprise on revenue, $1.18 billion versus $1.09 billion, was the biggest upside surprise in the company’s reporting history. And the outlook for this quarter’s revenue, $1,329 at the midpoint, was also the highest upside in forecast so far, thirteen percent.

Two heavy weeks of earnings reports have left stocks lower, the Nasdaq Composite Index closing down half a point the week ending November 14th, and five percent the week before. That is likely because of stocks hitting new 52-week and all-time high prices.

I compiled a list of thirty-two stocks that had the biggest declines and gains in the days and weeks following their earnings reports.

We’re past the biggest week of earnings season by market capitalization, and it’s worth reflecting upon what’s working and what’s not.

Five of the biggest names reported results back to back, Wednesday and Thursday, Alphabet, Microsoft, Meta, Amazon and Apple. All five showed healthy growth, but only Alphabet and Amazon saw a healthy pop in their stocks.

For Microsoft and Meta, the prospect of much higher spending is weighing on their shares. The patience that was displayed for Microsoft and Meta back in July seems to have evaporated.

I guess, when the stocks were only up twenty percent, mid-year, people were willing to indulge both companies. But, with gains of twenty-nine percent heading into these reports, investors showed less patience for both companies’ constant increase in spending.